New COVID-19 Stimulus In The Federal Budget 20/21 – Understanding Temporary Full Expensing & The Instant Asset Write Off Changes

– A range of new measures to support business and investment have been introduced in the new Federal Budget for 2020/2021. These are now active, having been announced on October 6th (‘Budget Night’), passing both houses on October 9th, and receiving Royal Assent on October 14th. Further changes have been made to the Instant Asset Write-off tax break, and the scheme has also been transformed and expanded under its new guise, ‘Temporary Full Expensing.’

-

The current Instant Asset Write Off is still in place for all assets up to $150,000 ex-GST purchased after March 12th 2020, and before 7.30pm on October 6th 2020. The install date for these assets has now been extended from December 31st, 2020 to June 30th, 2021.

-

The new ‘Temporary Full Expensing’ is available for new or used assets purchased after 7.30pm AEDT October 6th. There is now no upper limit on the price of assets. The install date for these assets is June 30th, 2022.

So what is Temporary Full Expensing?

Any business type with an aggregated turnover of up to $5 billion (ie. 99% of Aussie businesses) can write off the full expense of eligible brand new assets instantly. There is no threshold or limit to the number of brand new assets a business can claim. Additionally, small and medium-sized business (businesses with an aggregated turnover of less than $50 million) can write off the expense of eligible used assets instantly.

Temporary Full Expensing applies to all kinds of assets, and can include mowers, tractors, and implements. In fact, with the asset value now uncapped, it now applies to the entire KC Equipment range!

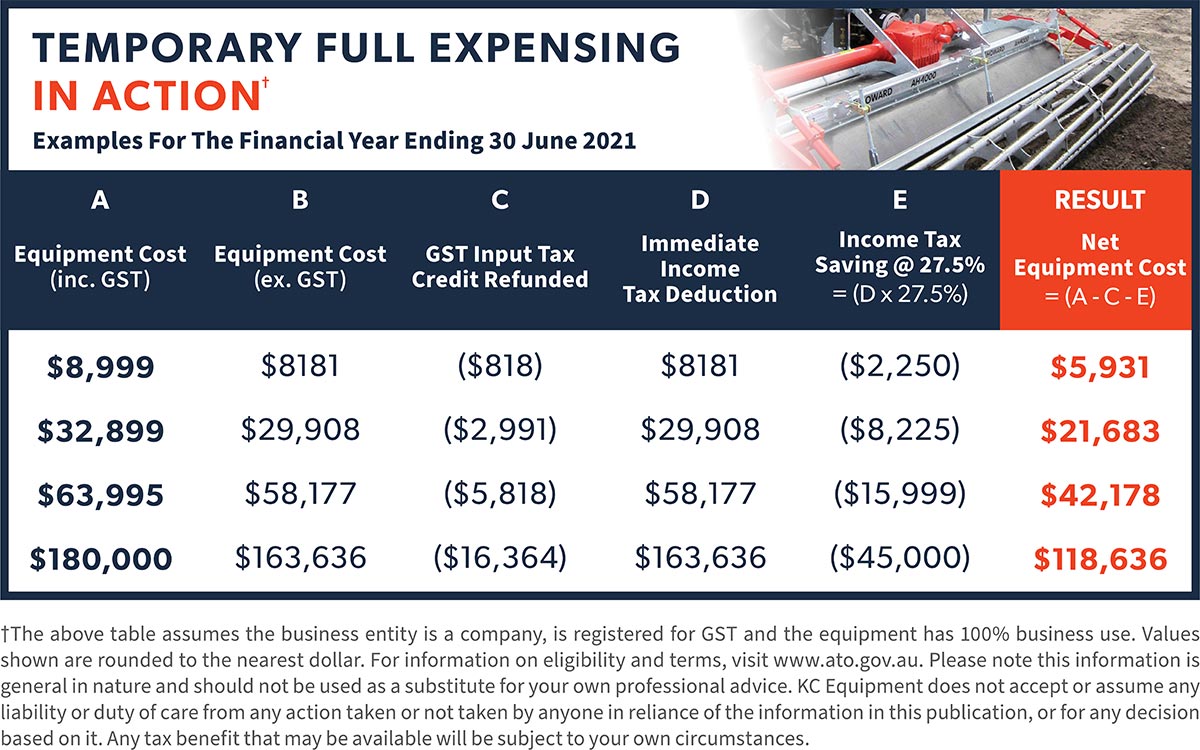

Like the Instant Asset Write-off scheme, the asset must be first used (or installed ready for use) by a strict deadline – in this case June 30th, 2022. Additionally, to claim the full deduction the asset must be used solely for business purposes. If you have a tax bill that you’d like to reduce, then you can get genuine savings on equipment using this incentive. Have a look at the examples below.

Depending on your business, there may be benefits to using an alternate depreciation structure, and some exclusions do apply to the immediate deductibility threshold. As always, we’d recommend seeking professional advice to understand any tax benefits that would apply to your own circumstances. You should not act, or refrain from acting, upon the general information presented here without obtaining specific professional advice.

As this scheme is still new, new information is still appearing on the ATO and other Government sites. We’d recommend visiting the Treasury website’s ‘Support for Businesses’ page for more information, along with the official Federal Budget website. Also of note in the budget is the phased increase in the SBE (Small Business Enterprise) turnover threshold, from $10 million to $50 million. This increases the availability of a number of small business tax concessions. Please refer to the ATO or seek professional advice for more information.

If you’d like to talk to KC Equipment about securing equipment utilising Temporary Full Expensing, then please visit our contact us page for details on your local branch, or enquire online.

KC Equipment services the Agricultural, Golf, Sports, Commercial and Residential grounds care industries with a huge range of equipment from the world’s leading manufacturers, including Massey Ferguson, Iseki, Kubota, and Jacobson. With over thirty years of experience, branches in Yatala, Lismore and Murwillumbah, and a huge parts and supplier network, KC Equipment can assist you with all aspects of your operation.

KC Equipment – for everything in your shed.

For any media enquiries, contact Jean-Paul Mollinger, Marketing Coordinator, on [email protected]

KC Equipment wishes all our fellow Australians the best for the challenges ahead. To find out the latest on our status during the COVID-19 response, please visit our Contact Us page.